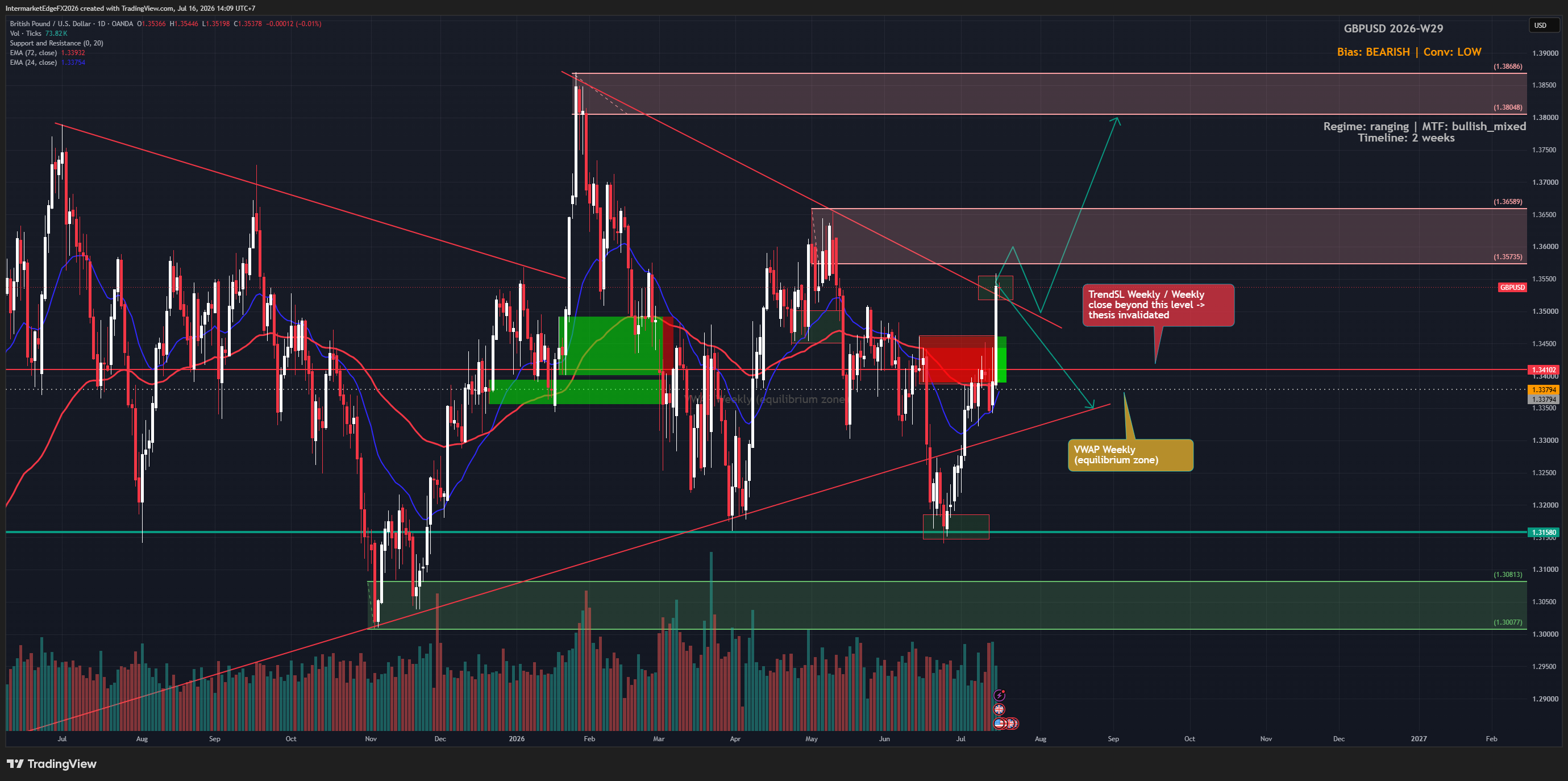

GBPUSD Week W29-2026: Softer US CPI Lifts Cable Briefly But Middle East Safe-Haven Flows and Fed Hawkishness Push Price Back Below 200-Hour MA Near 1.3364, Leaving Bulls and Bears Deadlocked

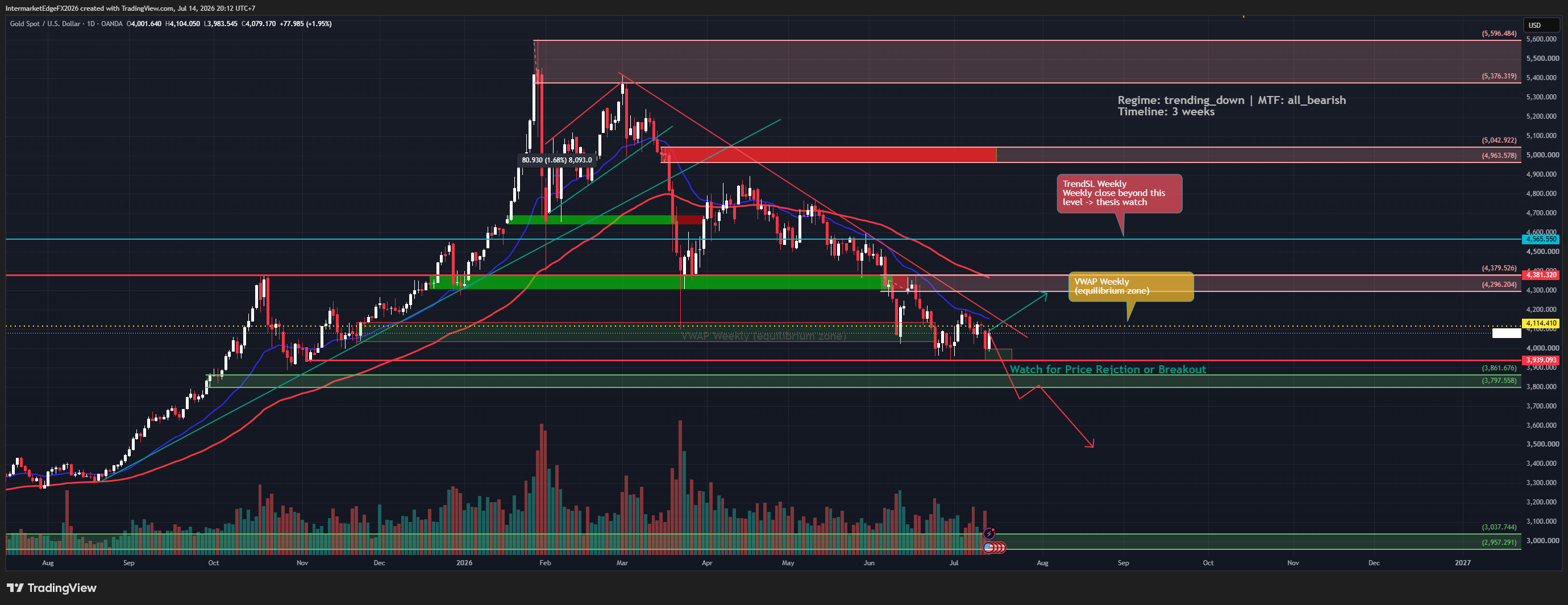

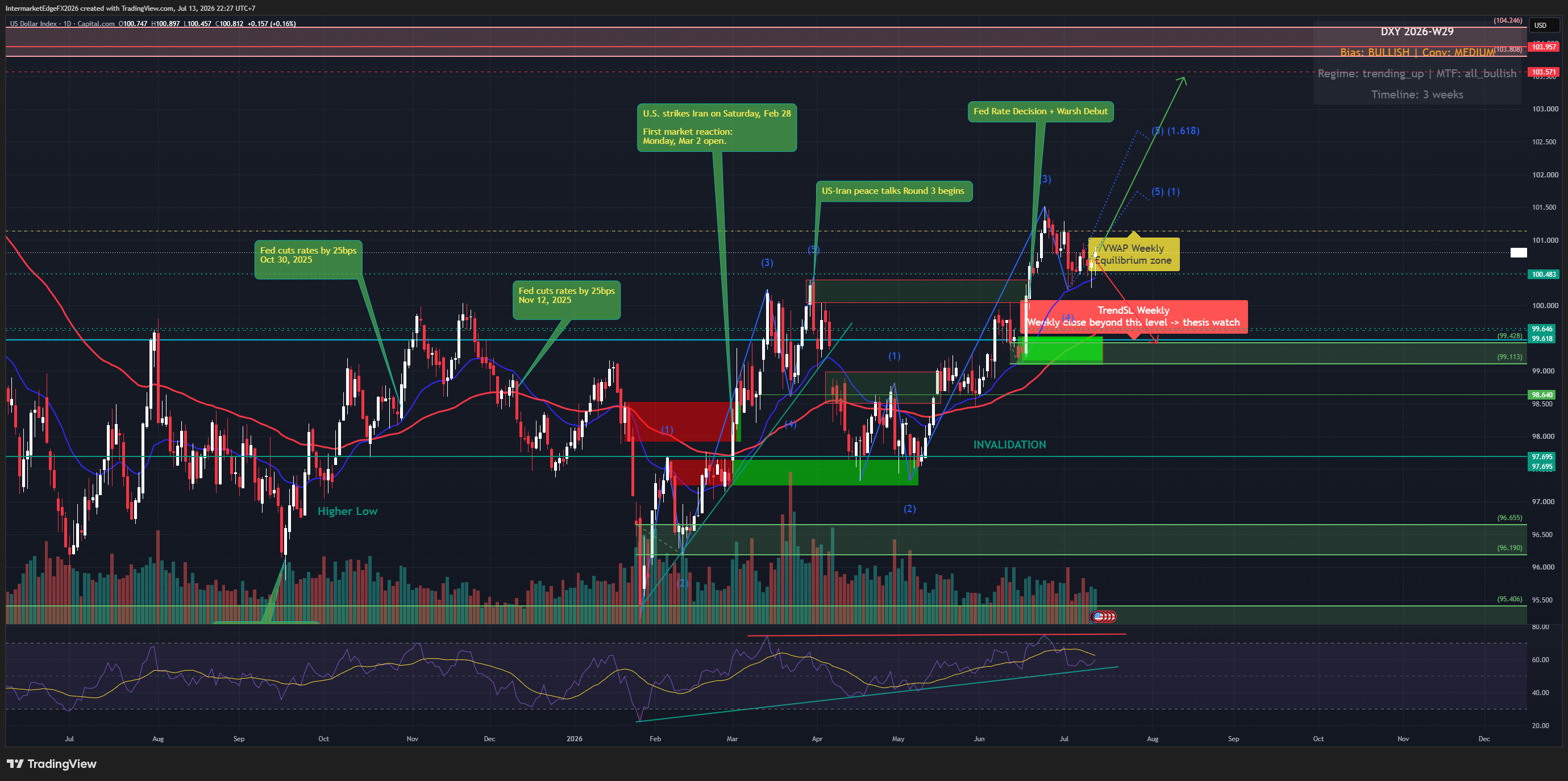

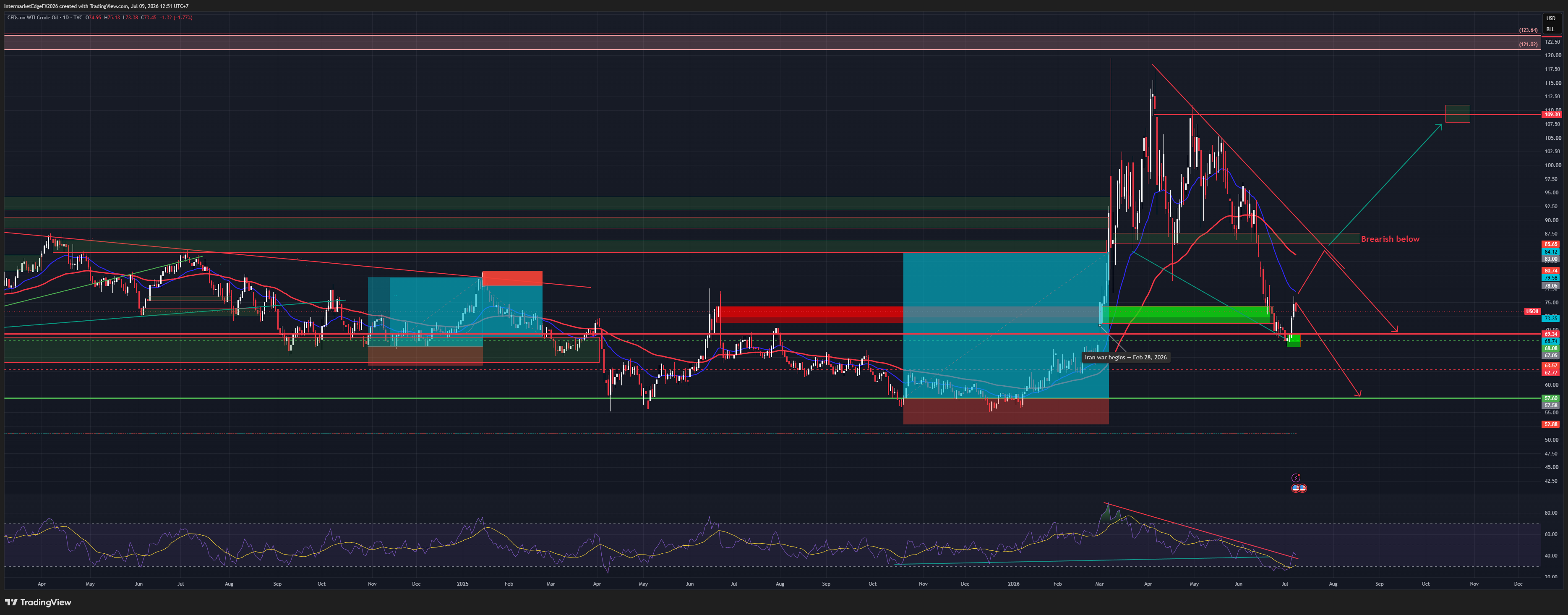

GBPUSD is caught between competing forces this week, and conviction on the bearish side is low — traders should size accordingly. On the USD side: June CPI printed softer than forecast, briefly sinking the dollar, but Fed's Waller immediately pushed back, warning that another hot core inflation print could force the Fed to consider raising rates. That keeps USD downside limited. US real yields remain elevated at 2.32%, and DXY bias sits at bullish/medium conviction — rate differential continues to favor USD structurally. On the GBP side: sterling rallied to a one-year high vs EUR and a 4-week high on reports of a Mahmood Treasury appointment and growing BoE rate-hike bets — both GBP-supportive. But Middle East tensions from US-Iran strikes lifted oil and triggered a USD safe-haven bid, dragging GBPUSD back below its 100/200-day MAs. Price is now testing the 200-hour MA near 1.3364 — a genuine battleground level. Regime is ranging (mean-revert implication). Price sits exactly at weekly VWAP (1.3379). COT, sentiment, and liquidity signals are all neutral — the bearish case rests almost entirely on macro and price data. MTF alignment is mixed, not cleanly directional. Key levels to watch: a weekly close above TrendSL at 1.3410 invalidates the bearish structure — exit shorts and reassess. Sustained price above VWAP (1.3379) is an early warning to reduce short exposure. Bottom line: structural lean is neutral-to-bearish, not outright bearish. Conflicting signals are real, not noise — avoid large directional positions until the 1.3364–1.3410 range resolves. -- Intermarket Edge