USDCAD Week W30-2026: Tariff Threats and Yield Spread Widening Push Pair to a One-Week Low, But VWAP at 1.40594 Keeps Bulls Cautiously Alive

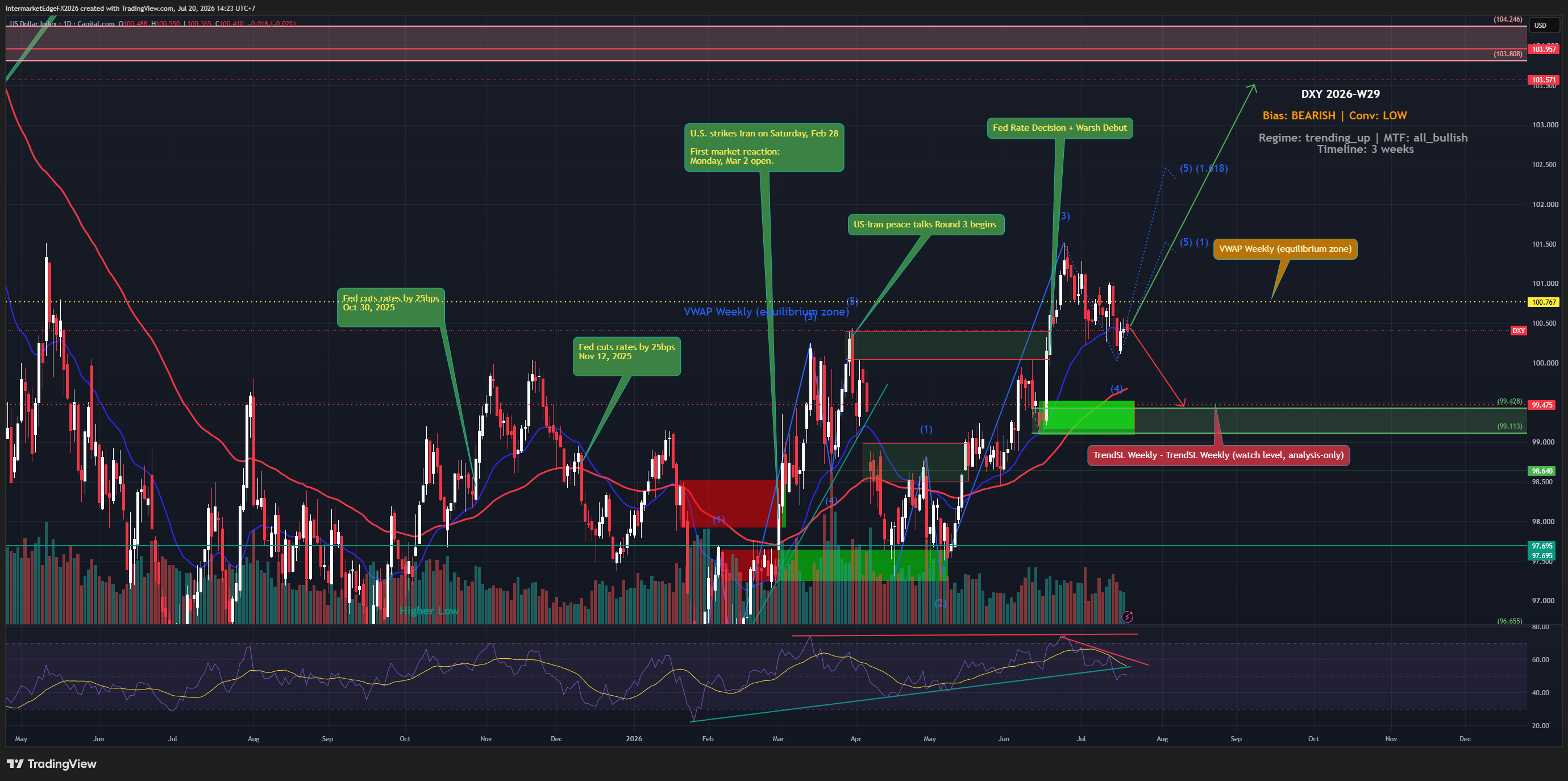

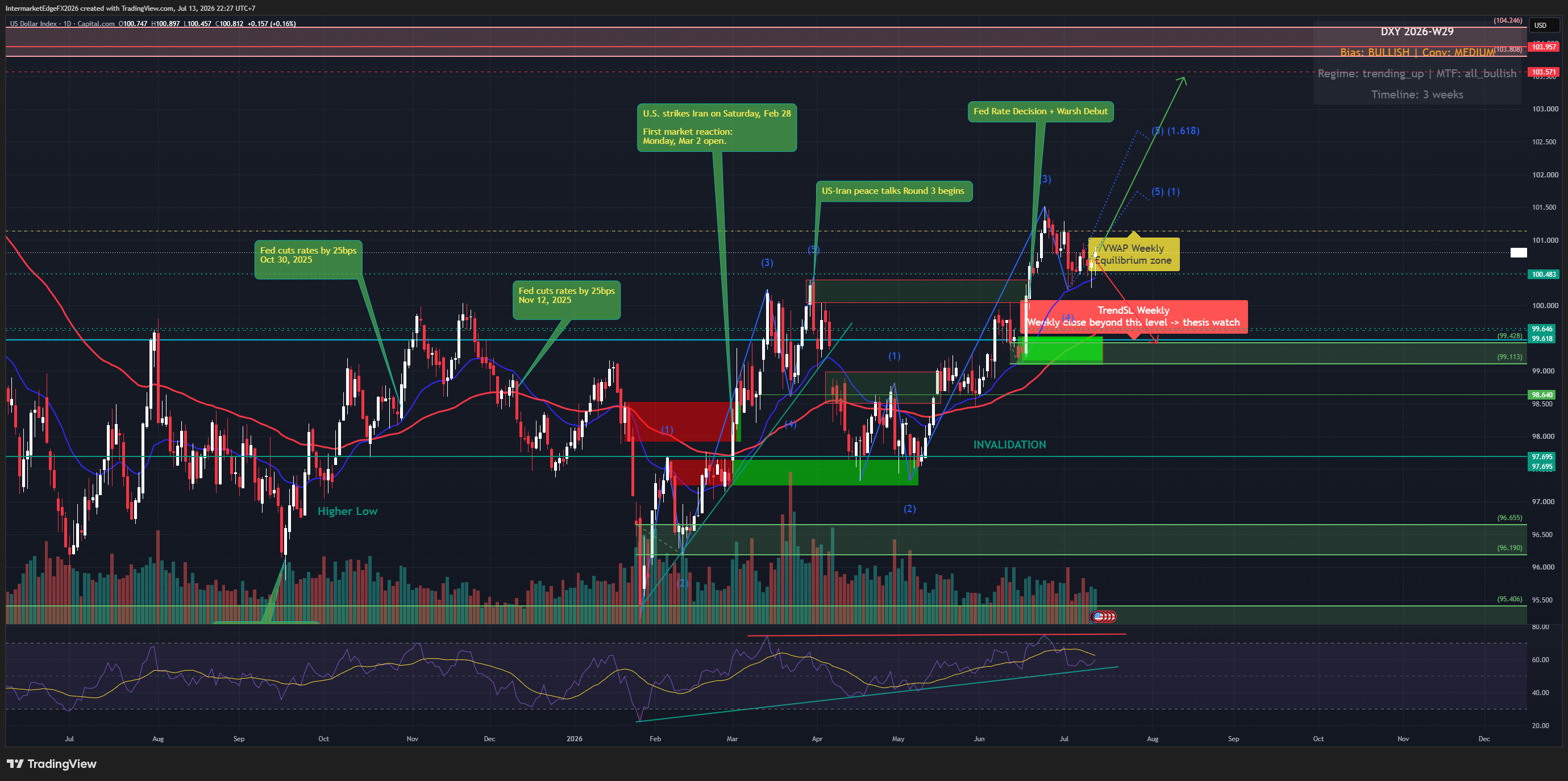

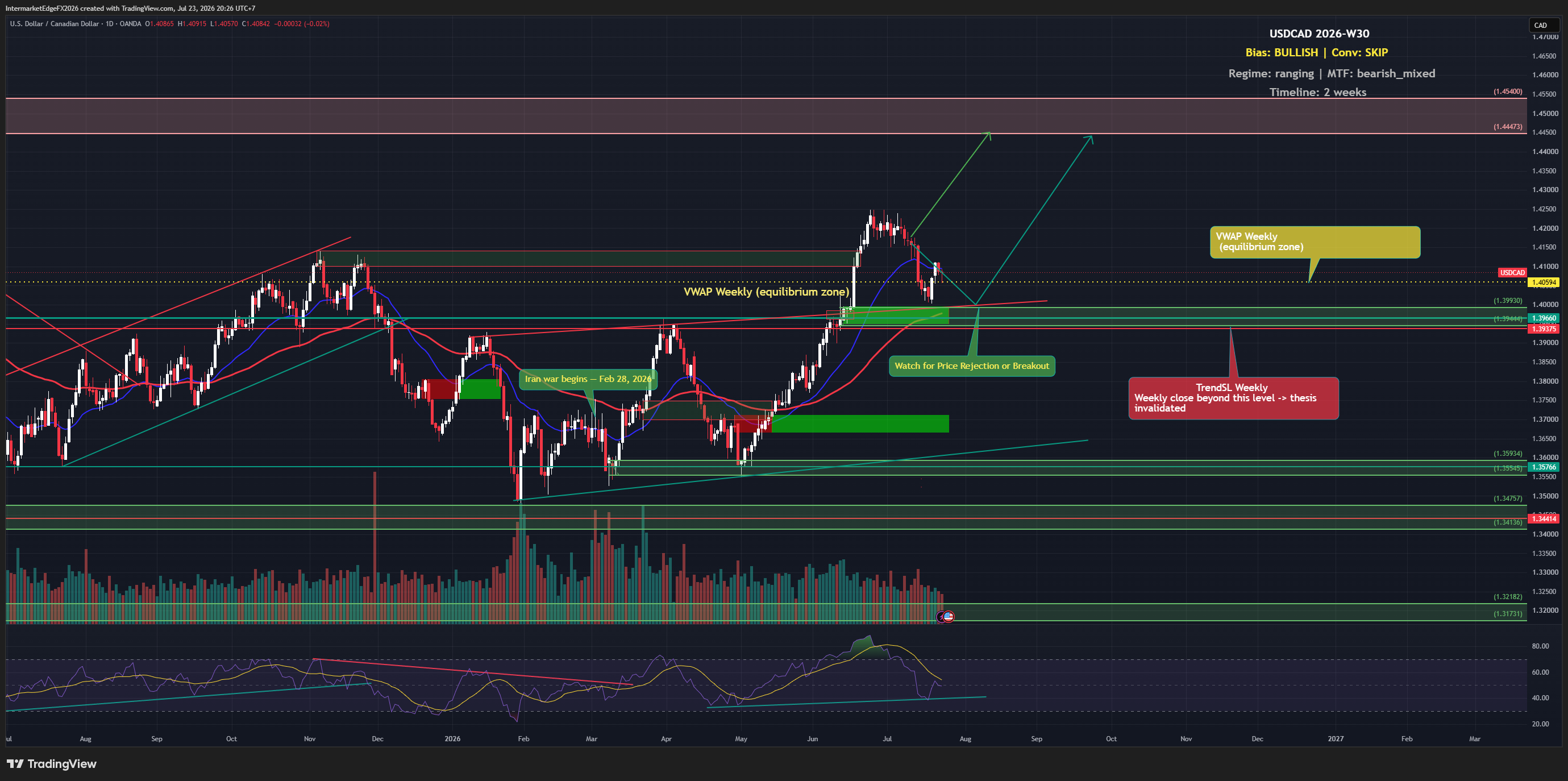

USDCAD is trading at 1.4083 (as of 2026-07-23T13:15 UTC, yfinance near-realtime), marginally above the weekly VWAP of 1.4059 and well above the trend support at 1.3937. The regime is ranging with a mean-reversion implication — not a trending environment. The news backdrop is mixed. The Canadian dollar briefly strengthened on rising benchmark yields, but then hit a one-week low as yield spreads widened following renewed U.S. tariff threats. Ottawa's response was sharp — PM Carney called the latest tariff move a USMCA violation, while USTR Greer countered that Canada is offering better deals to third parties. Separately, USD is finding a bid from U.S.-Iran tensions pushing Brent higher — which cuts both ways for USDCAD since oil strength typically supports CAD. The bullish bias rests on two pillars: COT positioning (net bullish) and macro fundamentals — the Fed remains hawkish, real yields are elevated at 2.37%, and the rate differential favors USD. However, conviction is low; price, liquidity, and sentiment signals are all neutral. A TGA drain is flagged as a partial offset, simultaneously supporting risk assets and capping USD upside. Critical override risk: a sustained oil rally would strengthen CAD and could neutralize the entire setup regardless of rate differentials. Structural levels to watch: a weekly close below VWAP (1.4059) warrants size reduction; a close below TrendSL (1.3937) invalidates the bullish structure entirely. Given low conviction, keep sizing conservative and wait for price confirmation before adding directional exposure. -- Intermarket Edge